The Refractories Market is segmented by Product Type (Non-clay Refractory and Clay Refractory), End-user Industry (Iron and Steel, Energy and Chemicals, Non-ferrous Metals, Cement, Ceramic, Glass, and Other End-user Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers market size and forecast for Refractories in volume (kilotons) for all the above segments.

Market Overview

Refractories Market was valued at 50,000 kiloton in 2020 and is expected to grow at a CAGR of over 5% during the forecast period 2021-2026.

Due to COVID-19, numerous countries were in lockdown, which significantly affected the global economy, the economic and industrial activities came to a temporary halt, and the refractories market also witnessed its repercussion in terms of both productions and demand from the end-user industries, such as iron and steel, cement, energy and chemicals, ceramics, etc.

- Over the medium term, the major factors driving the market studied are the strong growth of iron and steel production in the emerging countries and the increase in the production of non-ferrous materials. The refractories are used for internal lining applications in iron steel and non-ferrous productions.

- Moreover, high demand coming from the glass industry is the major factor driving the growth.

- On the flip side, due to the increasing environmental awareness, government agencies and environmental agencies across the world are laying down the guidelines regarding the usage and disposal of refractories. This is likely to hinder the market growth.

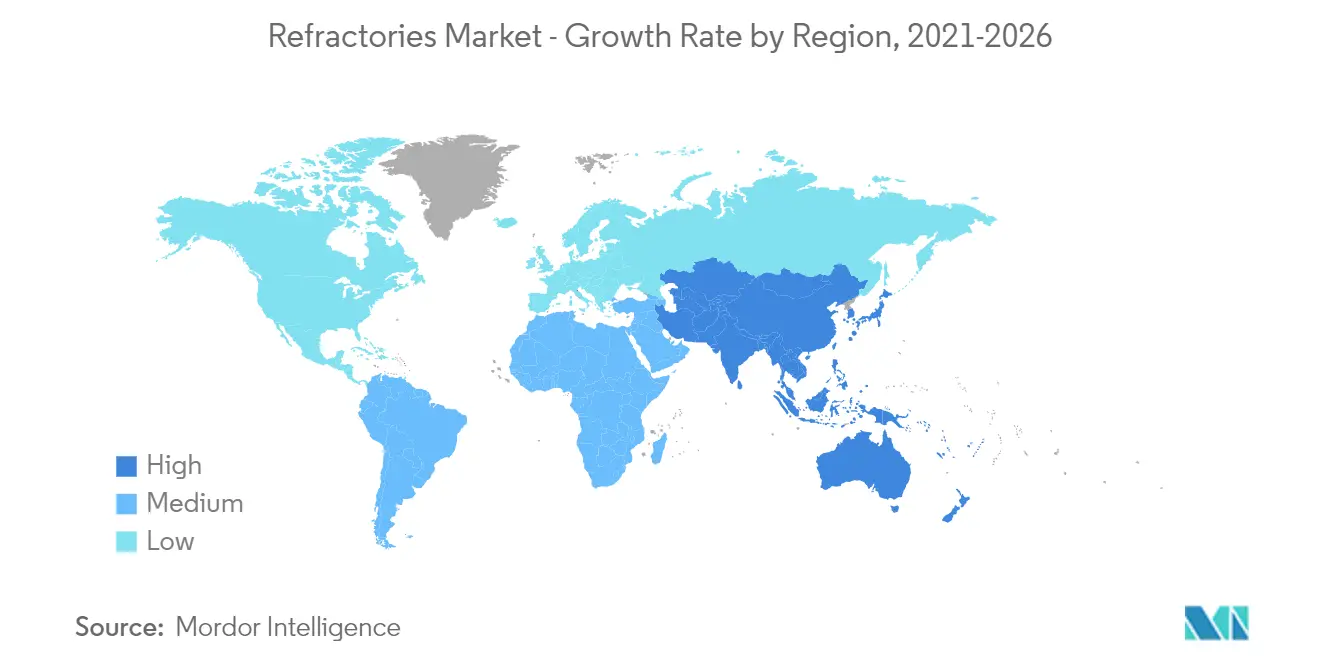

- The Asia-Pacific region is likely to dominate the market and is expected to have the highest CAGR. Emerging countries, like China, Russia, Mexico, and South Africa, are investing heavily in large-scale infrastructure projects, which are expected to significantly boost the growth of the iron and steel industry.

Scope of the Report

A refractory or refractory material is a material that, at high temperatures, is resistant to decomposition by heat, pressure, or chemical attack and retains strength and form. Refractories are used as a primary material for internal linings in large industrial equipment for their safe, low-maintenance, and cost-effective operations. The refractories market is segmented by product type, end-user industry, and geography. By type, the market is segmented into non-clay refractories and clay refractories. By non-clay refractories, the market is segmented into magnesite brick, zirconia brick, silica brick, chromite brick, and other non-clay refractories. By clay refractories, the market is segmented into high alumina, fireclay, and insulating refractories. By end-user industries, the market for refractories is segmented into iron and steel, energy and chemicals, non-ferrous metals, cement, ceramic, and glass. The report also covers the market size and forecasts for the refractories market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kiloton).

Key Market Trends

Increasing Demand from the Iron and Steel Industry

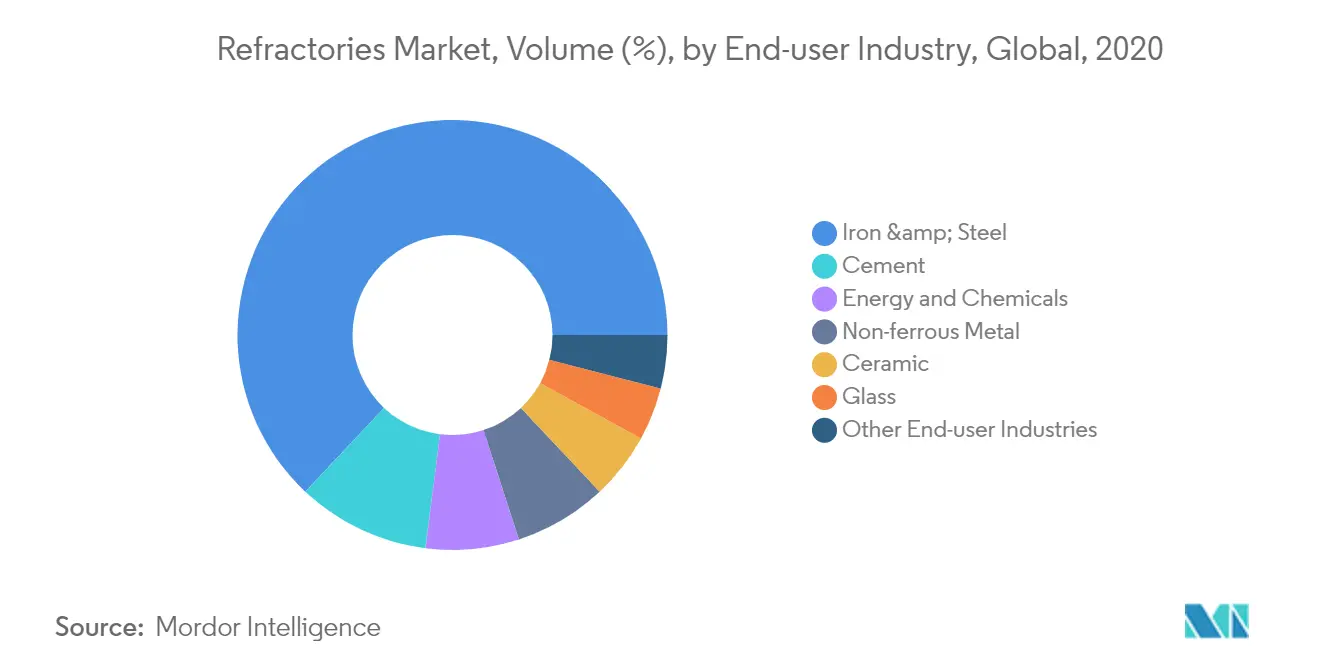

- The iron and steel industry is the major end user of refractories, which accounts for around 60% of the market. These materials can withstand high temperatures, ranging from 260°C (500°F) to 1850°C (3400°F), without any major change in their physical properties.

- The major applications of refractories in the iron and steel industry include usage in internal linings of furnaces to make iron and steel, in furnaces for heating steel before further processing, in vessels for holding and transporting metal and slag, in the flues or stacks through which hot gases are conducted, and other applications.

- According to the World Steel Association, the global steel demand reached about 1.76 million metric ton in 2019, and it was projected to reach 1.81 million ton by 2021, registering a growth of about 1.7%. This indicates the demand prospect prevailing in the global market, which serves as instrumental in driving steel production activities.

- According to World Steel Association, global crude steel production in 2020 reached 1,864 million metric ton, down by 0.9% compared to 2019 due to COVID-19.

- In terms of consumption, Asia-Pacific is currently the largest consumer of refractories in the iron and steel industry, followed by Europe and North America. In North America, the United States is expected to witness the highest growth rate in the consumption of refractories in this industry during the forecast period.

- In the European Union, a mild recovery in demand for steel continues while improving the economic sentiments and investment conditions. However, uncertainties in the political landscape, related to the refugee crisis and Brexit, are some of the risks to the economic condition. The demand for steel in the region is anticipated to grow at a slow pace over the forecast period.

- All the aforementioned factors are expected to drive the global market during the forecast period.

To understand key trends, Download Sample Report

China to Dominate the Asia-Pacific Region

- In the Asia-Pacific region, China is the largest economy in terms of GDP. The country witnessed about 6.1% growth in its GDP during 2019, even after the trade disturbance caused due to its trade war with the United States. The economic growth rate of China in 2020 was initially expected to be moderate as compared to the previous year. China dominates the refractories market in terms of consumption and production due to the local availability of raw materials, such as magnesite.

- Additionally, they are available at cheaper costs as compared to other producers. The iron and steel industry consumes the largest portion of refractories, globally and in China as well.

- The iron and steel industry consumes the largest portion of refractories, globally, and in China as well. Industrial restructuring and the decreased consumption rate of refractories for per ton of steel have impacted the demand for refractories in China between 2013-16. However, growing construction activity is creating demand for the production of iron and steel in the country and have been driving the growth of the refractories market in the recent times.

- China is largest steel producer worldwide with a crude steel production volume of nearly 996 million metric tons in 2019. In the first half of 2021, Chinese steel mills have churned out nearly 12% more crude steel compared to the same period in 2020. According to world steel org, China produced 86.8 Mt in July 2021, down 8.4% on July 2020. However, it produced 93.9 Mt in June 2021which which was a increase of 1.5% as compared to June 2020. The Chinese government has ordered the steel mills to ensure the annual steel output in 2021 remains on par with 2020 levels This huge demand for steel in the country projects market opportunities for refractories.

- The Chinese automotive manufacturing industry is the largest in the world, with a production share of just over 28% in 2019. According to the China Association of Automobile Manufacturers (CAAM), the automotive production decline by about 2% in 2020. The country produced 25,225,242 units in 2020, which declined from 25,750, 650 units in 2019. However, in Q1, 2021, the production reached 6,352,028 which increased 81.7% over Q1 2020. The manufacturing activities are picking up pace, driving the demand for metals and thus driving the market of study.

- In China, the construction industry grew at a strong pace in 2020, but the growth was restricted due to the pandemic situation. The construction sector has supported the economic growth in the country whenever major slowdowns occurred. The country has the largest construction market in the world, encompassing 20% of all construction investments, globally. The country is investing USD 1.43 trillion in the next five years till 2025 in major construction projects. According to National Development and Reform Commission (NDRC), the Shanghai Plan includes the investment of USD 38.7 billion in the next three years. Despite the decrease in the production of cement since last half decade, the aforementioned factors are expected to increase the demand of metals, cements and other products related to the market thus creating a positive market outlook for refractories.

- Overall, the demand for refractories in China and Asia-Pacific region, is expected to grow at a significant rate during the forecast period.

To understand geography trends, Download Sample Report

Competitive Landscape

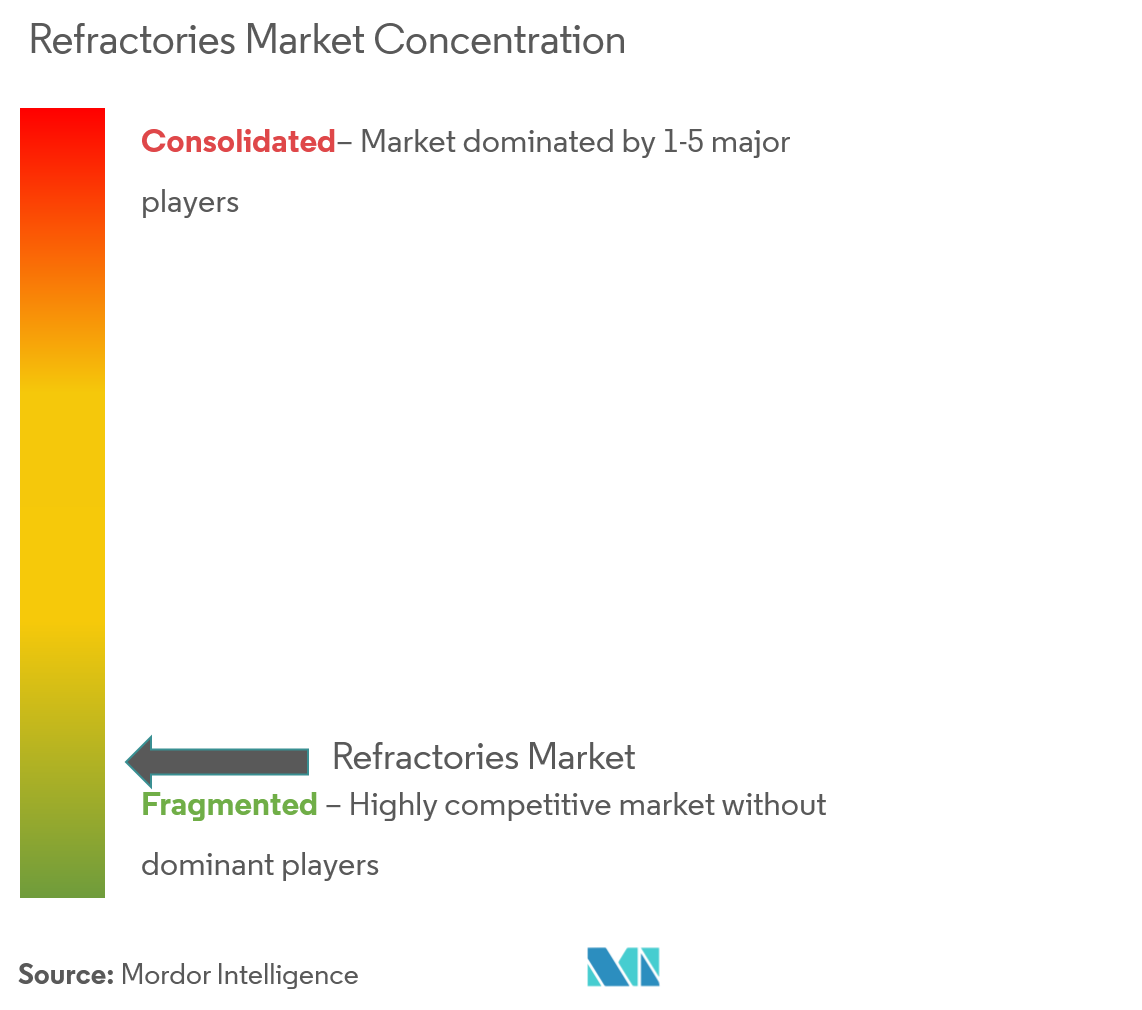

The global refractories market stands to be fragmented in nature, where the top five companies cater to about 34%-35% of the global market demand. The major players include RHI Magnesita GmbH, Vesuvius, Krosaki Harima Corporation, Shinagawa Refractories Co. Ltd, and Saint-Gobain, among others.

Recent Developments

- In May 2021, ArcelorMittal Refractories,a part of the ArcelorMittal Group, entered into a partnership agreement with Krosaki Harima Corporation. The companies will carry out tasks to optimize production capacities and expand ArcelorMittal Refractories` portfolio of refractory products, using Krosaki Harima`s manufacturing technology.

- In March 2021, Refratechnik Group and Höganäs Borgestad Group entered into a strategic agreement for the supply of refractory products.

- In August 2020, Imerys signed an agreement for the acquisition of a majority stake of about 60% of Haznedar Group, a Turkish-based high-grade monolithic refractory and refractory bricks manufacturer serving the iron and steel, cement, and petrochemical industries.